Off Shore Binary Options

Offshore binary options are often discussed as if they were just another high risk trading niche. That framing is too soft. The real issue is not only product risk. It is that offshore binary options, as sold to retail customers online, have been linked for years with unregistered platforms, fake broker conduct, blocked withdrawals, and outright fraud. The CFTC states plainly that binary options can be traded on registered U.S. exchanges, but many websites, social media posts, ads, and videos promote unregistered binary options trading platforms, often operated by offshore companies committing fraud. That is the right place to start, because it separates lawful market structure from the version most retail traders actually encounter online.

For traders and investors with basic knowledge, the confusion usually comes from mixing three separate questions. First, is the product itself legitimate in some jurisdictions. Second, is the platform offering it lawfully registered where it needs to be. Third, even if the platform exists as a company somewhere offshore, does that give the customer any real protection when money is stuck or misconduct starts. Those are not the same question. An offshore operator may talk like a broker, market like a social media trading app, and look polished enough to pass for a proper venue. That still does not answer whether the customer has a real counterparty, enforceable rights, or any workable route to recover funds when things go wrong. The SEC’s investor education materials on binary options make the same basic point: some operators may not comply with securities laws, may be unregistered, and may simply be trying to scam you.

What binary options are and why offshore firms like them

A binary option is a yes or no proposition on a future market condition. The CFTC describes it in exactly those terms. If the condition is met at expiry, there is a fixed payout. If not, the result is zero or a defined loss of stake depending on the structure. That simplicity is a sales gift. The product can be explained quickly, marketed visually, and framed as easier than ordinary options, margin trading, or outright directional speculation. For a retail audience that knows markets only at a basic level, “up or down by this time” sounds cleaner than Greeks, spreads, or position management. That does not make the product automatically fraudulent, but it does make it very easy to package in misleading ways.

Offshore firms like the product for the same reason casino operators like fast games. The trade duration can be short, the interface can be simple, and the customer can be encouraged to repeat decisions quickly. The FCA, when it imposed a permanent ban on the sale of binary options to retail consumers in the UK, said the product posed a risk of consumer harm and estimated that the ban could reduce harm and also reduce the risk of fraud by unauthorised entities claiming to offer these products. ESMA took a similar line at EU level, prohibiting the marketing, distribution, or sale of binary options to retail investors because of significant investor protection concerns caused by the characteristics of the product. That language matters. Regulators were not describing a niche product that merely needed better disclosure. They were describing a product and distribution pattern associated with serious retail harm.

For offshore operators, binary options also solve a commercial problem. They allow a website or app to present a vivid trading experience without needing to prove much about execution quality, depth of market, or pricing transparency in the way that a more mature trading venue might. The customer sees timers, price movement, payouts, and account balances. That is often enough to create the impression of a functioning financial platform. In a lawful, regulated setting, those mechanics sit inside a framework of registration and oversight. In an offshore solicitation model, they can sit inside little more than a payment funnel wearing a trading costume. The CFTC and SEC joint alert says complaints about internet based binary options platforms fall into at least three categories: refusal to credit customer accounts or reimburse funds, identity theft, and manipulation of software to generate losing trades. That is not a routine product warning. It is a description of how the business can fail at the most basic level.

The line between lawful venues and the offshore solicitation model

There is an important legal distinction that gets lost in everyday conversation. Binary options are not automatically illegal everywhere. The CFTC says they can be traded on registered U.S. exchanges. The trouble begins when retail customers are steered away from registered venues and toward unregistered websites, apps, or “brokers” that appear to offer the same thing but sit outside the regulatory framework applicable to the customer. That is where the phrase offshore binary options usually stops meaning a lawful cross border service and starts meaning an unregistered solicitation model aimed at retail money. You can read more about were binary options are legal, where they are unregulated and where the promotion of binary options is banned by visiting BinaryOptions.net.

In the United States, the CFTC has long warned against off exchange binary options trades and says many offshore companies engaged in commodity binary options transactions are not registered with the CFTC and are best avoided entirely. It adds that when companies operate offshore, investors have even fewer protections and are at greater risk of being targeted for fraud. That is unusually direct guidance. It is not saying customers should proceed carefully. It is saying avoidance is the better policy. The reason is practical as much as legal. Even if the offshore entity exists on paper, the customer is usually much further away from effective supervision, dispute resolution, and asset recovery.

Europe took a harder line for retail distribution. ESMA’s product intervention measures prohibited the marketing, distribution, or sale of binary options to retail investors in the EU, and the FCA later made the UK retail ban permanent. Those steps were based on investor protection concerns, not merely on licensing technicalities. So when an offshore site markets binary options across borders to retail users, it is often targeting people in places where mainstream regulators have already decided the product should not be sold to them at all. That alone should change how the offer is read. The issue is not only whether the firm is offshore. It is that the firm may be offering a product into markets where retail protections were tightened specifically because harm was recurring.

The SEC’s enforcement work also shows this is not an abstract concern. In 2021, a federal court entered judgments against owners and operators of three overseas binary option brokers that targeted U.S. investors. That matters because it demonstrates that overseas binary option operations have not just been the subject of warnings. They have also been the subject of enforcement tied to targeting retail investors across borders. The trouble for victims is that enforcement after the fact is not the same as easy recovery. A lawsuit years later is cold comfort when a trading account has already turned into an email argument with no money coming back.

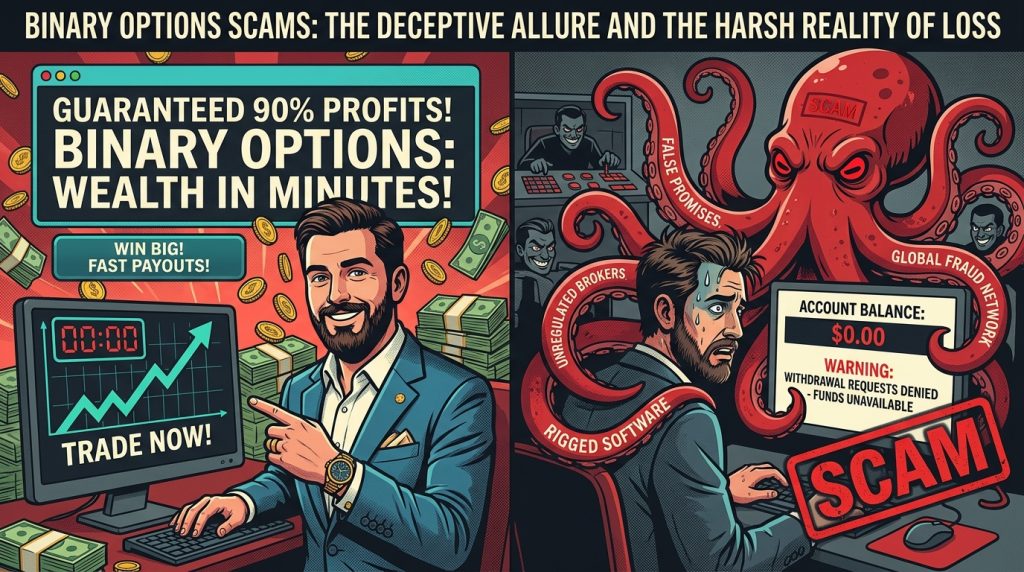

Why offshore binary options have such a bad reputation

The reputation comes from the pattern of harm, not from forum gossip. The CFTC and SEC investor alert on binary options and fraud lays out a grim set of complaint categories: failure to credit accounts properly, refusal to reimburse funds, identity theft, and software manipulation producing losing trades. The CFTC’s broader binary options fraud page says many online binary options trading platforms operate in violation of the law and highlights the same issues. These are not edge cases around fees or service quality. They go to the core of whether the platform is functioning honestly at all.

Withdrawal friction is one of the most repeated complaints. In a legitimate trading relationship, a customer can lose money because the trade went wrong. In a scam relationship, a customer can “make money” on screen and still fail to withdraw anything. That is a different category of risk. The platform balance stops being evidence of funds and becomes part of the marketing display. The CFTC materials specifically warn about refusal to credit customer accounts or reimburse funds. Once that pattern appears, discussion of strategy becomes almost irrelevant. The central issue is no longer payout structure or trading skill. It is whether the platform ever intended to honour customer balances in the first place.

Identity theft is another reason the category deserves more caution than a normal speculative product. The SEC’s investor education page on binary options warns that operators may not comply with securities laws and may actually be trying to scam you, while the joint CFTC SEC alert includes identity theft among the main complaint types. In practice that means the victim may lose more than a deposit. They may also have handed over passport copies, banking details, proof of address, card information, and other personal data to an operator whose main asset is distance. Once that happens, the financial loss can spread beyond the original account.

Then there is platform control. Offshore binary options operators often control the customer interface, the quoted prices or strike presentation, the trade confirmation path, and the withdrawal gate. The joint alert’s reference to software manipulation generating losing trades is especially important here. In ordinary market speculation, there is always a chance that the market simply moved against you. In a manipulated platform, the house may be deciding more than the customer realizes. That possibility is one reason regulators distinguish lawful exchange traded products from unregistered internet platforms. In the first case, loss may reflect market risk. In the second, loss may reflect platform abuse.

Cross border enforcement weakness makes all of this worse. The CFTC’s off exchange warning says investors have even fewer protections when companies operate offshore. That is the dry version. The lived version is that customers often end up dealing with a company incorporated in one place, operated from another, using payments through a third place, soliciting into a fourth place, with support staff who may not be where they claim to be at all. Even if regulators later act, distance, cost, jurisdiction, and missing records can make recovery difficult. That practical weakness is part of the model. Offshore structure is not always chosen because the weather is better. Sometimes it is chosen because accountability is worse.

How the scam usually works now

The modern offshore binary options funnel rarely begins with a hard sell for binary options. More often it begins with a social media post, short video, copied article, fake endorsement, or trading education style page. The CFTC’s materials on fraud consistently point to online promotions, social media, and unregistered platforms. The user is drawn in by a familiar promise: quick trading, easy interface, low starting deposit, “analyst” guidance, or passive help from an account manager. The binary options label may appear early or only after the user is already in conversation.

After the first click, the handoff matters. The customer is moved into chat, a call, or a direct account signup where sales pressure can be tailored. The platform may show a few early wins or even allow a small first withdrawal to build trust. This is a common fraud pattern across fake trading sites, and the CFTC’s scam site warning signs for forex, options, and similar products focus heavily on registration failures and other indicators that the website is a fraud. The point is to create enough confidence that the second deposit is larger than the first. That is when the tone changes. More funds are needed for better payouts, account upgrades, taxes, verification, or unlocking profits. By then the customer is debating account procedures instead of asking whether the venue is real.

Bonuses and promotional credits also play a role. Even when framed as generous marketing, they can function as traps by tying withdrawals to turnover requirements or by giving support staff a reason to argue that funds are not yet eligible to leave. Regulators’ repeated warnings about refusal to reimburse funds and blocked accounts fit this pattern, even where the specific excuse varies. The customer thinks the problem is paperwork. Often the problem is that the business only works while deposits move inward.

Copied identities add another layer. A site may borrow names, licenses, or general styling from legitimate firms. The SEC warns broadly that bad actors may operate as unregistered broker dealers or exchanges, and the CFTC advises users to check registration status as part of avoiding binary options fraud. If a customer relies only on a polished website or a claimed office location, the check is too weak. In this part of the market, looking professional has never been the same as being regulated.

Do offshore binary options firms’ interests collide with the trader’s interests

Yes, and the collision is often sharper than in ordinary retail brokerage. In many offshore binary options setups, the firm is not simply charging a commission for neutral access. It is often controlling the product terms, customer interface, and payout conditions while standing in an adversarial commercial position to the customer. Even where the operator calls itself a broker, the practical relationship can look more like a house taking the other side under rules it largely controls. That means conflict of interest is not a side concern. It sits at the center of the model.

A lawful retail trading provider can still have conflicts, of course. But offshore binary options frequently add two more layers. The first is weak or absent regulation where the customer lives. The second is direct platform control, including the possibility of software manipulation or arbitrary withdrawal barriers. The CFTC and SEC alert’s reference to manipulated software and blocked reimbursements shows why this is worse than the usual “the broker wants volume” concern seen in other leveraged products. Here, the firm may benefit not only from customer losses in trading, but also from limiting whether customer gains can ever be realized.

So do their interests collide with the trader’s interests. Often yes, completely. The trader wants fair pricing, honest settlement, and withdrawal of available funds. A bad offshore operator may want continuing deposits, low payout, and maximum control over exit. That is not a mild commercial mismatch. It is a structural clash dressed up as a trading service.

What traders should check before sending money

Start with registration and entity verification. The CFTC says the best way to avoid binary options fraud is to check the company’s registration status and, where relevant, the broker’s registration status too. Registration is not a guarantee against fraud, but it helps weed out firms operating outside U.S. law. That is the minimum screen, not an advanced one.

Then check jurisdiction and product legality. If major regulators in the customer’s region have banned or prohibited retail marketing of binary options, an offshore solicitation should not be read as a clever workaround. It should be read as a warning sign. ESMA and the FCA both took intervention action because of consumer harm and fraud risk.

Finally, watch how the money moves. Unusual payment methods, pressure to deposit more for release of profits, and any friction around withdrawals should be treated as decisive red flags, not customer service issues that may sort themselves out later. The regulator complaint pattern on offshore binary options has been too consistent for too long to dismiss those signs as minor admin trouble.

Closing

Offshore binary options are not just a speculative product category with a rough reputation. In retail practice, they have been repeatedly associated with unregistered platforms, blocked withdrawals, identity theft, manipulated software, and cross border enforcement problems. Regulators in the U.S., EU, and UK have spent years drawing the same line: lawful venues exist in narrow regulated settings, but the offshore online version marketed to retail customers is where fraud risk becomes hard to separate from the business itself. The website may look modern. The problem is old.